Twipe Insights

What the 2026 Digital News Report Means for Your App and Editions Strategy

Every year when the Reuters Institute Digital News Report is released, LinkedIn fills up with charts, researchers share threads, and outlets publish their takes (we’re no different). This year, Ezra Eeman went a step further and turned the part of the data into an interactive site. The DNR, in other words, has its moment — and rightly so. 97,520 respondents across 48 markets is not a dataset you ignore.

Most coverage will walk you through the headlines. We wanted to do something more specific: take the findings and ask what they mean, practically, for European publishers and their apps and editions strategy. Here’s what the data says is holding, shrinking, and shifting.

What’s holding

The platform shift documented in this year’s DNR is a historical first: people are getting more news from social & video platforms (54%) than from news websites and apps (52%).

But the pace of this shift is not geographically uniform. Direct access still leads in Western and Northern Europe. Audiences in this region still have a habit of going directly to news outlets they trust.

Which brings me to the second thing that is holding: brand-level trust. It’s a fact that overall trust in news has dropped to 37%, the lowest point since the Reuters Institute began measuring it in 2015. That sounds catastrophic, and in aggregate it is.

But the report distinguishes carefully between trust in news as a concept and trust in specific outlets people know and use regularly. The latter is proving resilient. In short, people have lost faith in “the news.” They have not lost faith in the outlets they know.

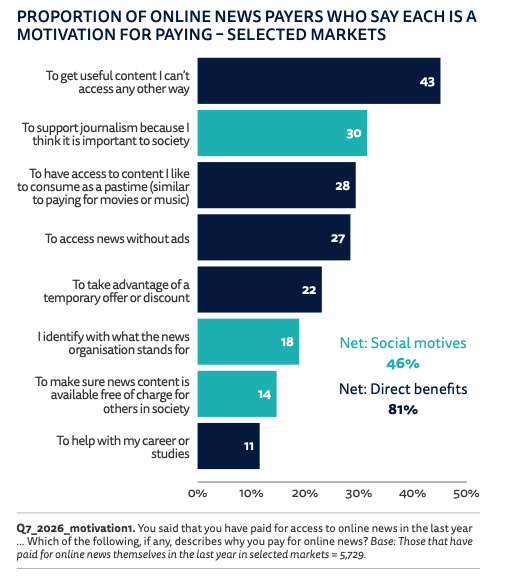

Both brand-level trust and the European habit of going directly to publishers make the case for investing in owned digital products. The 17% of people who pay for online news are motivated primarily by two things:

- access to content they cannot get elsewhere (43%),

- and a values-based desire to support journalism (46%).

Neither motivation is served by a social feed or a video algorithm. Both require a direct relationship with a brand the reader has consciously chosen. That is the audience already in your app, and understanding what drives them should shape product decisions.

What’s shifting

The European advantage is real, but it would be a mistake to read it as stable. The more you dig into this year’s data, the clearer it becomes that the conditions underpinning direct access are eroding.

Audience habits are what are shifting most. The assumption that younger people behave differently while older cohorts stay loyal has been a quiet comfort for European publishers for years. But the report finds the move toward social and video as a main news source is happening across all age groups — and crucially, older audiences are adopting the habits of younger audiences, not the reverse.

Nowhere is this clearer than in video. 77% of the global sample now consume online news video every week, across every market the report covers. But they are not consuming it on publisher platforms. Video consumption on publishers’ own sites and apps has fallen ten percentage points since 2021.

Within this shift, though, is an opportunity many publishers are trying to capture. A quarter of those who follow news on YouTube watch for more than 20 minutes at a time, and a fifth use the platform specifically for live broadcasts. This is not short-form snacking. It is an engaged, substantial appetite for exactly the kind of journalism publishers produce. The product question here is whether video can be built into owned digital experiences in ways that give readers a reason to stay on your platform rather than defaulting to YouTube or TikTok.

What’s shrinking

The hardest part of this year’s report for many European publishers to sit with is what it implies, indirectly, about digital editions. The data doesn’t address editions directly, but the picture it paints of audience behaviour makes the strategic implications hard to avoid.

56% of people aged 18 to 24 have never regularly read a newspaper. The production cycles, the scheduled format, the sense of a complete and bounded daily read: these are habits shaped by a medium this cohort has little relationship with. Digital editions replicate that format faithfully. For readers who grew up with print, that familiarity is genuinely valuable. For everyone else, it is a format that requires learning a behaviour they have never had.

What makes this harder to dismiss is the finding about older audiences. If the edition audience were simply ageing in place — loyal but not growing — that would be a manageable challenge. But the report shows older audiences are also shifting toward younger habits. It is shrinking from both ends.

None of this is an argument to abandon editions. They serve a loyal, intentional, paying audience that values the curated, complete experience they offer. That audience is worth retaining. What editions cannot do is carry the growth ambitions of a product strategy. The practical question is not whether to have editions — it is whether they define your app or sit within a broader experience that can do things editions cannot.

The Telegraph is an example of a European publisher building a whole suite of experiences within their app. They used to have a separate live news and edition app, but have since merged into on Modular News App which incorporates various experiences: a lifestyle section, finance, enetertainment, a newsletter module, podcasts, and puzzles, alongside the edition and live news modules. The app users have eight more sessions per week than web users and show six more retention points at 30 days.

Key takeaways for European publishers

- Protect your direct relationship. European audiences still come directly to publishers they trust. That habit is your most valuable commercial asset — and it is worth investing in the product experience that reinforces it.

- Lean into brand trust. Overall trust in news is falling, but trust in specific, known outlets is holding. Publishers with strong brands can benefit from this.

- The app’s experiences are the product. Editions are a retention tool, not a growth engine, so build apps with a wide-range of experiences. Publishers like The Telegraph have shown what it looks like to build a full experience — live news, editions, lifestyle, podcasts, puzzles — into a single owned environment.

Other Blog Posts

Stay on top of the game

Join our community of industry leaders. Get insights, best practices, case studies, and access to our events.

"(Required)" indicates required fields